Written in a CEO-friendly, reflective tone, as if typed by hand during an intense and uncertain market year.

Introduction: The Middle of the Storm

If Part 1 of this series described the build-up to 2008, then Part 2 captures the year as it was actually livedóin real time, without the benefit of hindsight. This was the phase where confidence began to fracture, volatility expanded, and assumptions were quietly abandoned.

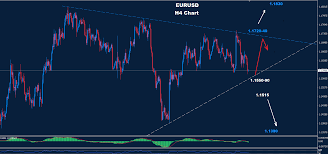

For managed forex accounts, 2008 was no longer about forecasting. It became about interpretation, adaptation, and survival. The EUR/USD pair stood at the center of this transformation, reflecting not only economic divergence, but emotional stress across global markets.

This section focuses on the unfolding dynamics of 2008 and how professional managers navigated the most unstable phase of the year.

Shifting Narratives in the Currency Markets

At the start of 2008, the dominant narrative favored euro strength. The U.S. economy was slowing, the Federal Reserve was aggressively cutting rates, and the dollar was broadly viewed as vulnerable.

But markets rarely respect consensus for long.

As the year progressed, cracks began to appear in Europeís own financial system. Exposure to U.S. mortgage-backed securities, fragile interbank lending, and overleveraged balance sheets started to surface.

The EUR/USD pair began to reflect uncertainty rather than conviction.

For managed forex accounts, this meant reducing reliance on single narratives and increasing attention to real-time price behavior.

Volatility as the New Normal

One of the defining features of mid-2008 was volatility expansion. Daily ranges that once felt extreme became routine. Stop-loss levels had to be reconsidered. Holding periods shortened.

Volatility was no longer an event. It was the environment.

Professional managers adjusted by:

Reducing leverage

Scaling into positions

Taking profits earlier

Accepting missed opportunities

In this phase, capital preservation quietly became the primary objectiveóeven when performance reports still emphasized returns.

EUR/USD and the Breakdown of Technical Comfort

Many traditional technical tools struggled during this period. Trendlines were violated, support levels failed, and momentum indicators delivered late signals.

The EUR/USD pair produced numerous false breakouts, trapping both bullish and bearish traders.

Managed forex accounts that relied on rigid technical systems suffered. Those that treated technicals as context rather than commands adapted more effectively.

Price action, volatility structure, and liquidity conditions carried more weight than textbook patterns.

Fundamental Confusion and Policy Uncertainty

Central bank communication became increasingly influentialóand increasingly difficult to interpret.

The Federal Reserve continued to signal concern over growth and financial stability. The European Central Bank, initially more hawkish, began to soften its stance as economic data weakened.

For EUR/USD traders, this created conflicting signals:

Interest rate differentials lost clarity

Inflation concerns competed with recession fears

Policy expectations shifted rapidly

Managed accounts learned to treat central bank guidance as fluid, not fixed.

Risk Reduction as an Active Decision

One of the most difficult decisions for professional managers in 2008 was to trade less.

Clients often equate activity with competence. In reality, inactivity during unstable periods can be a sign of discipline.

Reducing exposure, holding cash, and waiting for clarity were strategic choicesónot failures of conviction.

This period reinforced an important lesson: not losing money is a position.

The Psychology of Uncertainty

Mid-2008 tested emotional resilience. News flow was relentless. Confidence eroded gradually, then suddenly.

For managed forex accounts, psychological pressure increased on multiple fronts:

Market unpredictability

Client expectations

Internal performance benchmarks

Managers who remained emotionally neutral made better decisions. Those who tried to force clarity into chaotic conditions often paid a price.

EUR/USD reflected this psychological tug-of-war, oscillating sharply without sustained direction.

Liquidity Signals and Early Warnings

While headlines lagged, currency markets began signaling deeper stress. Funding pressures, widening spreads, and unusual price behavior hinted at systemic issues.

The EUR/USD pair occasionally moved not on economic data, but on liquidity demand.

For experienced managers, these signals mattered more than forecasts. Liquidity always speaks first.

Managed accounts that paid attention adjusted exposure before the most dramatic phase of the crisis arrived.

Client Trust During Ambiguous Performance

Performance during this phase was mixed. Gains were possible, but consistency was difficult.

What separated strong managers from weak ones was communication.

Explaining why risk was reduced, why opportunities were passed, and why preservation mattered helped maintain long-term trust.

Transparency proved more valuable than short-term outperformance.

Preparing for the Unknown

By late summer 2008, it was clear that markets were approaching a breaking point. What form it would take was unknown.

Managed forex accounts that survived this phase did so by preparing for multiple scenarios rather than committing to a single outcome.

Flexibility replaced prediction.

EUR/USD was no longer a trend trade. It was a risk barometer.

Strategic Lessons From the Middle Phase

Several lessons emerged clearly from this period:

Volatility changes behavior

Narratives expire faster than expected

Liquidity matters more than valuation

Reducing risk is an active skill

Emotional control is a competitive advantage

These lessons shaped how managed forex accounts approached the final and most intense stage of 2008.

Final Thoughts: Between Confidence and Collapse

Part 2 of the EUR/USD story is about transition. It captures the moment when certainty faded but panic had not yet fully arrived.

For managed forex accounts, this was the testing ground. Decisions made here determined who would survive what came next.

The EUR/USD outlook during this phase was not about direction. It was about durability.

In Part 3, we examine how this durability was ultimately tested when the crisis reached its peak.

Summary:

Forex Managed Accounts update: Where the EUR/USD is heading in 2008! Why the USD weakend in 2007, where US Economy is going and how the US presidential elections may affect the financial markets!

Keywords:

Forex Managed Accounts,forex,economy,

Article Body:

What Rate Cuts Can Be Expected

The US Fed has not exactly been forthcoming in its rate cuts; rather, it lowered rates very reluctantly in 2007. It has given only what the currency markets have already priced in. The basic reason for their hesitation is the desire to contain inflation ? the very same concern that weighs heavily on all other central banks in the world. The Fed wants to make certain inflation remains under control. Doing that has been more difficult because of the high energy prices coupled with the weaker dollar. Thankfully, indications of energy prices reaching $100 per barrel are no longer in circulation.

The market expects the Fed to further ease interest rates another 25 to 50bp lower; however, this is not the only option. They may want to further explore their other options, including the Term Auction Facility they introduced in December. But these options, including a cut in the discount rate, are limited especially since LIBOR rates have remained at high levels. Even as late as December, Treasuries posted one-day increases that were the highest seen in the last three years.

Who Else Might Make A Play

In the final two months of 2007, the crumbling markets were shored up by massive investments from sovereign funds. Temasek Holdings, owned by Singapore, invested $4.4 billion in Merrill Lynch; state-owned Abu Dhabi Investment Authority plowed $7.5 billion into Citigroup; and, China Investment Corporation invested $5 billion in Morgan Stanley. Sovereign wealth funds have been in existence since the mid-twentieth century. From an estimated $500 billion total size in 1990, these funds are now thought to be worth $3 trillion. The states of Norway, Singapore, the U.A.E., Saudi Arabia, Kuwait and China have between them an estimated $2 trillion available for immediate spending. Given eight more years, these funds may have total capital of $12 trillion, continuously built up from their natural resources and foreign exchange reserves. Investments from sovereign wealth funds have ? and probably will continue ? to be significant factors in helping the US financial markets recover.

How the 2008 US Presidential Elections May Affect Financial Markets

The historical trend shows more bullishness for the US dollar when Republicans gain leadership than Democrats. Whether this trend will hold depends on how close the 2008 elections will turn out. The Stock Traders Almanac makes the general observation that election years show modestly positive growth in the US stock market. In the last five decades, election years have shown a 9.2% average gain in the Dow Jones index.

Managed Forex Accounts ñ EUR/USD Outlook 2008 (2/3)

•

Tinggalkan Balasan